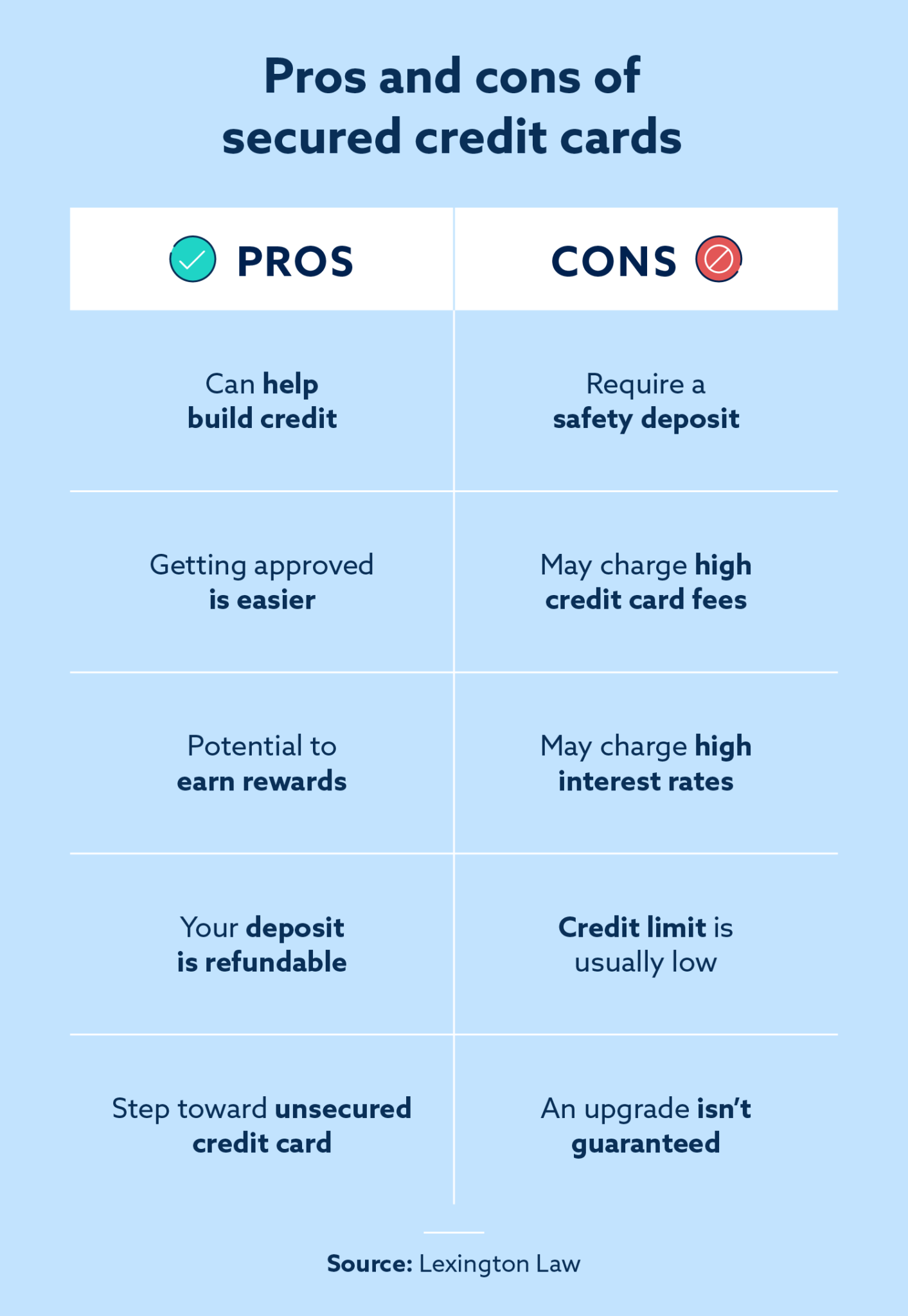

Related Content

Nevertheless, it isn’t impractical to be eligible for home financing having a simple credit file, but you will must keep working harder to acquire a lender. Possibilities become taking a cosigner, qualifying to have an authorities mortgage program otherwise organizing to own merchant financing.

Consult a loan provider

A home loan company normally feedback the money you owe and you can enable you to determine if you really have a high probability within qualifying getting a great home loan. Loan providers can also consider what’s named “solution credit” recommendations, just like your history of and also make rent, electric and you may insurance policies money promptly. Both a beneficial option credit rating, plus your money, may be enough to provide home financing. About, a mortgage lender can present you with advice with the building the borrowing in order to sooner or later qualify for a loan.

Turn to Uncle sam

Some authorities financial applications reduce strict credit requirements and could desire regarding a position records and income than simply credit score. This type of government apps is loans insured because of the Federal Housing Management, U.S. Service out-of Farming Rural Innovation and Department of Pros Affairs. For every program features its own certification procedure and you can limits into kind of property that can easily be bought, therefore it is important to communicate with a mortgage lender otherwise housing counselor regarding your choices. That benefit of of many bodies home loan apps is that they wanted either no down-payment otherwise a highly reduced you to definitely.

Entice a good Cosigner

Without having the credit to help you be eligible for home financing on your own, you could potentially query anyone having good credit so you can cosign your loan application. New cosigner will have to be individuals which have a good credit score and you will adequate money to pay for your home loan repayments for those who default towards the the loan. Defaulting into the good cosigned mortgage is notably ruin the connection with the fresh new cosigner, no matter if, therefore it is important to seriously consider whether or not getting a mortgage are worthy of which risk.

Seller Money

Only a few home loans require you to sort out a lender or home loan company. You may be capable get a property which have provider or holder financial support. In vendor funding, the vendor generally acts as the lender, granting the cash advance usa San Acacio address application purchasing the house or property, setting-up the new terms of the borrowed funds and event costs. Since supplier takes on a great deal of exposure with these types of mortgage, the loan terms and conditions have a tendency to establish a fairly high downpayment and you may may not assist you the new 15 to thirty years that old-fashioned mortgage loans give you to pay off the whole financing. However, it can be possible for one to make your borrowing from the bank throughout this time to be able to refinance your property not as much as a antique loan system.

Enhance Downpayment

Without having much of a credit score but carry out keeps serious cash, you happen to be able to find that loan by simply making a great high deposit. Certain traditional lenders and home loans might be able to find you that loan whenever you can manage an enormous advance payment. There are even “hard-money lenders” which are experts in getting finance to people who don’t be eligible for almost every other home loan apps. A challenging-loan provider will most likely wanted a very high deposit and you can costs a higher rate interesting, not, so it is crucial that you opinion this package cautiously.

- Coldwell Banker United Lenders: Ought i Score a loan which have Less than perfect credit?

- MSN A house: How to get home financing In the place of a credit score

- Nolo: Supplier Resource: How it works home based Conversion process

- Chicago Tribune: The real truth about Tough-Currency Finance

- : Help FHA Money Make it easier to

- : Mortgage brokers: Pros

- Bankrate: Top Causes Never to Co-Sign on that loan

Lainie Petersen produces on the company, real estate and private finance, attracting to your twenty five years experience with posting and you may training. Petersen’s works seems in Money Crashers, Promoting with the Masses, plus in Walmart Development Now, a web log to own Walmart services. She keeps a good master’s training from inside the library technology regarding Dominican College.